Summary and print methods for "Renouv" objects

summary.Renouv.RdSummary method for "Renouv" objects representing 'Renouvellement' (POT) fitted models.

Usage

# S3 method for class 'Renouv'

print(x,

digits = max(3L, getOption("digits") - 3L),

...)

# S3 method for class 'Renouv'

summary(object,

correlation = FALSE,

symbolic.cor = FALSE,

...)

# S3 method for class 'summary.Renouv'

print(x,

coef = TRUE,

pred = TRUE,

probT = FALSE,

digits = max(3, getOption("digits") - 3),

symbolic.cor = x$symbolic.cor,

signif.stars = getOption("show.signif.stars"),

...)

# S3 method for class 'summary.Renouv'

format(x,

...)Arguments

- object

-

An object with class

"Renouv". - x

-

An object of class

"summary.Renouv", i.e. a result of a call tosummary.Renouv. - correlation

-

Logical; if

TRUE, the correlation matrix of the estimated parameters is returned and printed. - coef

-

Logical. If

FALSE, the table of coefficients and t-ratios' will not be printed. - pred

-

Logical. If

FALSE, the table of return periods/levels will not be printed. - probT

-

If

FALSE, the \(p\)-values for the t-tests will not be printed nor displayed. - digits

-

the number of significant digits to use when printing.

- symbolic.cor

-

logical. If

TRUE, print the correlations in a symbolic form (seesymnum) rather than as numbers. - signif.stars

-

logical. If

TRUE, ‘significance stars’ are printed for each coefficient. - ...

-

Further arguments passed to or from other methods.

Details

print.summary.Renouv tries to be smart about formatting the

coefficients, standard errors, return levels, etc.

format.summary.Renouv returns as a limited content as a

character string. It does not embed coefficients values nor

predictions.

Value

The function summary.RenOUV computes and returns a list of

summary statistics concerning the object of class "Rendata"

given in object. The returned list is an object with class

"summary.Renouv".

The function print.summary.Rendata does not returns anything.

Examples

## use Brest data

fit <- Renouv(Brest)

#> Special inference for the exponential case without history

#> Warning: uncertainty on the rate not taken into account yet in the exponential with no history case

summary(fit)

#> o Main sample 'Over Threshold'

#> . Threshold 30.00

#> . Effect. duration 147.62 years

#> . Nb. of exceed. 1289

#>

#> o Estimated rate 'lambda' for Poisson process (events): 8.73 evt/year.

#>

#> o Distribution for exceedances y: "exponential", with 1 par. "rate"

#>

#> o No transformation applied

#>

#> o Coefficients

#>

#> Estimate Std. Error t value

#> lambda 8.7318791 0.243209905 35.90265

#> rate 0.0850335 0.002368447 35.90265

#>

#> Degrees of freedom: 2 (param.) and 1289 (obs)

#>

#> o Inference method used for return levels

#> "chi-square for exponential distribution (no historical data)"

#>

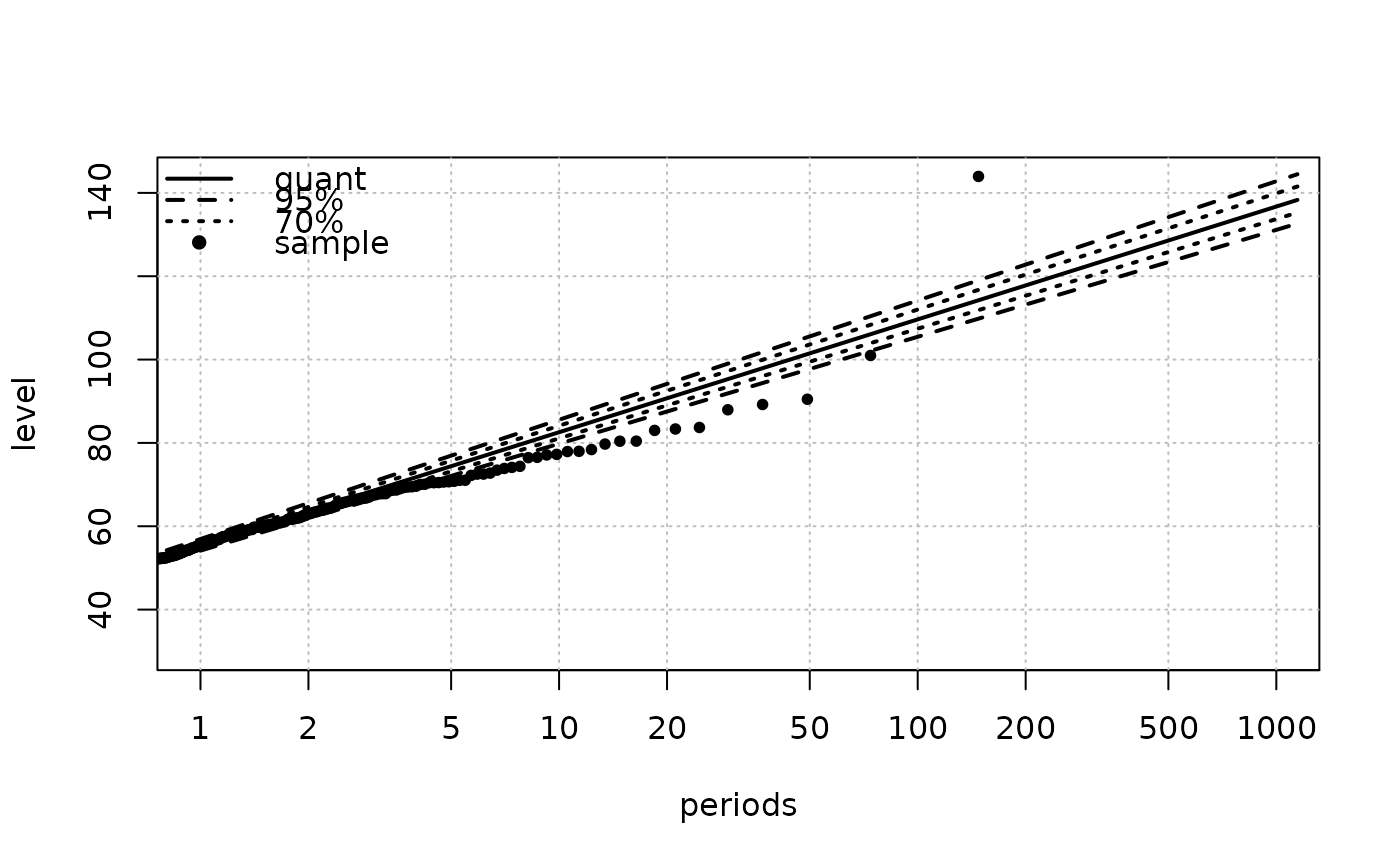

#> o Return levels

#>

#> period quant L.95 U.95 L.70 U.70

#> 33 10 83 80 86 81 84

#> 35 20 91 88 94 89 93

#> 39 50 101 98 106 99 104

#> 41 100 110 105 114 107 112

#> 43 200 118 113 123 115 120

#> 46 300 123 118 128 120 125

#> 48 400 126 121 131 123 129

#> 49 500 129 123 134 126 131

#> 51 600 131 125 136 128 134

#> 52 700 133 127 138 130 136

#> 53 800 134 129 140 131 137

#> 54 900 135 130 141 133 139

#> 55 1000 137 131 143 134 140

#>

#>

#> o no 'MAX' historical data

#>

#> o no 'OTS' historical data

#>

#> o Kolmogorov-Smirnov test

#>

#> Asymptotic one-sample Kolmogorov-Smirnov test

#>

#> data: OTjitter(y.OT, threshold = 0)

#> D = 0.02115, p-value = 0.6115

#> alternative hypothesis: two-sided

#>

#>

#> o Implied model for block maxima

#> Distribution: gumbel

#> Coeffficients

#> loc scale

#> 55.48385 11.76007

summary(fit)

#> o Main sample 'Over Threshold'

#> . Threshold 30.00

#> . Effect. duration 147.62 years

#> . Nb. of exceed. 1289

#>

#> o Estimated rate 'lambda' for Poisson process (events): 8.73 evt/year.

#>

#> o Distribution for exceedances y: "exponential", with 1 par. "rate"

#>

#> o No transformation applied

#>

#> o Coefficients

#>

#> Estimate Std. Error t value

#> lambda 8.7318791 0.243209905 35.90265

#> rate 0.0850335 0.002368447 35.90265

#>

#> Degrees of freedom: 2 (param.) and 1289 (obs)

#>

#> o Inference method used for return levels

#> "chi-square for exponential distribution (no historical data)"

#>

#> o Return levels

#>

#> period quant L.95 U.95 L.70 U.70

#> 33 10 83 80 86 81 84

#> 35 20 91 88 94 89 93

#> 39 50 101 98 106 99 104

#> 41 100 110 105 114 107 112

#> 43 200 118 113 123 115 120

#> 46 300 123 118 128 120 125

#> 48 400 126 121 131 123 129

#> 49 500 129 123 134 126 131

#> 51 600 131 125 136 128 134

#> 52 700 133 127 138 130 136

#> 53 800 134 129 140 131 137

#> 54 900 135 130 141 133 139

#> 55 1000 137 131 143 134 140

#>

#>

#> o no 'MAX' historical data

#>

#> o no 'OTS' historical data

#>

#> o Kolmogorov-Smirnov test

#>

#> Asymptotic one-sample Kolmogorov-Smirnov test

#>

#> data: OTjitter(y.OT, threshold = 0)

#> D = 0.02115, p-value = 0.6115

#> alternative hypothesis: two-sided

#>

#>

#> o Implied model for block maxima

#> Distribution: gumbel

#> Coeffficients

#> loc scale

#> 55.48385 11.76007